Cui Bono? New Manhattan Chemtrail Project Motives (Part 2)

A paper by meteorologist Loren W. Crow appeared in the most referenced early weather modification report; 1958’s “Final Report of the Advisory Committee on Weather Control.” In reference to money that might be made from additional hydroelectric power generation, her paper reads, “An annual [cloud] seeding project which covers 1,000 square miles might cost only $20,000 and have a reasonable chance of producing additional water worth $100,000. Another project with a target area of only 500 square miles might cost $50,000 per year to operate but the value of a small increase in additional water might be worth $1,000,000.” She’s writing about making, on a short-term basis, five to twenty times the money invested. Those are some healthy returns!

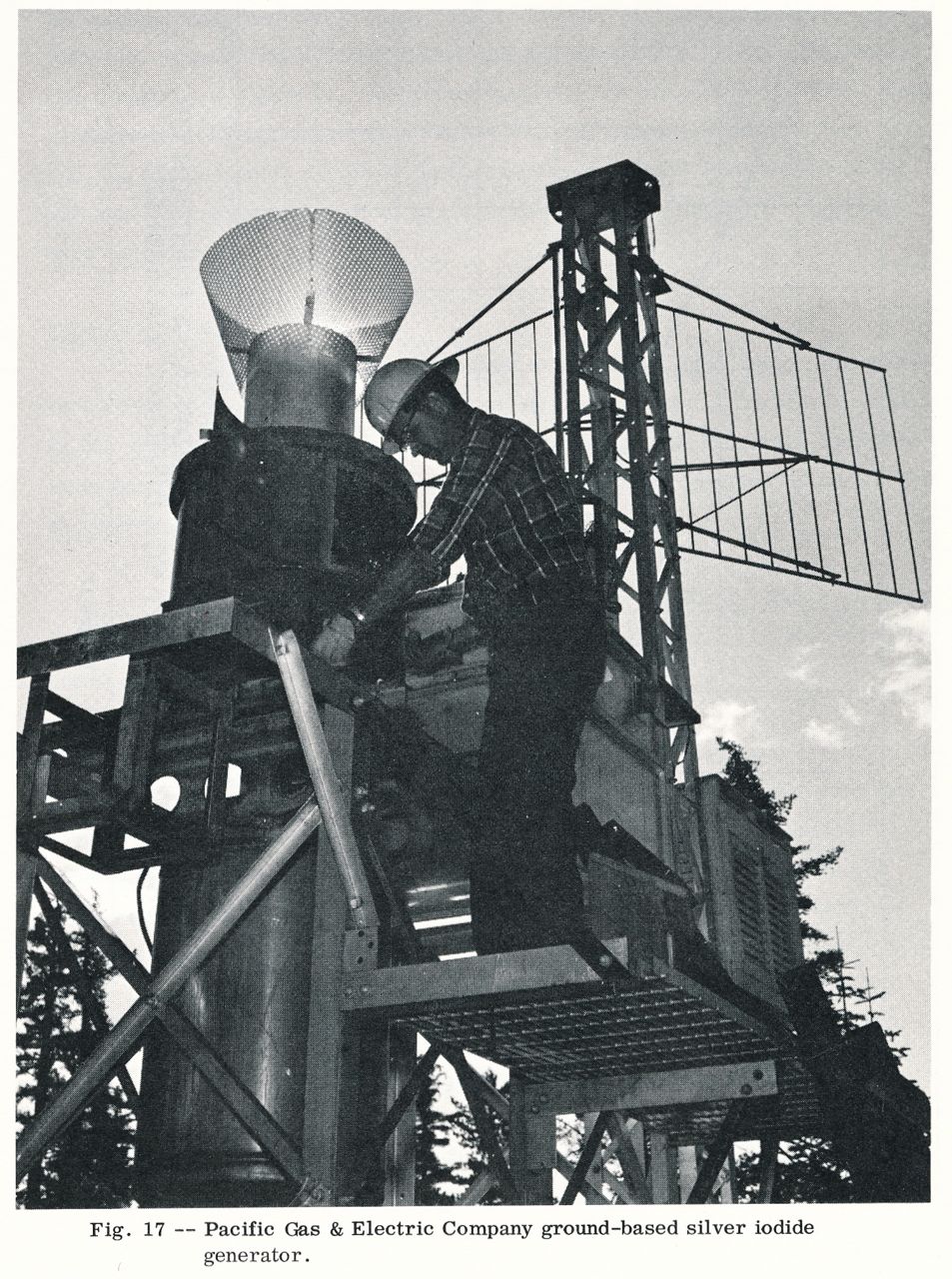

Pacific Gas and Electric (PG&E) did an initial study, the results of which were published in a 1966 paper titled “Weather Modification and the Operations of an Electric Power Utility: The Pacific Gas and Electric Company’s Test Program.” They were operating ground based silver iodide generators in order to enhance mountain snowpack and thus increase hydroelectric power. PG&E found average cost/return ratios of 1:5.56.

The Congressional Research Service’s senior specialist on the subject wrote in a 1978 report, “In a 1969 study, the Travelers Research Corp. estimated that run-off from the entire Connecticut River basin might be increased by about 2 million acre-feet (15 percent) per year through a weather modification program. It was calculated that this increment of water would cost $2.30 per acre-foot, or $4,600,00 annually. The report also stated that net benefits of $1,400,000 from municipal water supply, and $2,600,00 from supply of cooling water for thermal electric generating stations and increased flow for hydroelectric power generation might be realized by the 1980’s.” We will shortly have more about the Travelers.

Any way you slice it, if you’re in this line of work, it makes plain old dollars and cents to modify the weather. Do you really think that all these people and organizations would have been so heavily invested in weather modification over the years if it didn’t work? As far as the efficacy of conventional weather modification and the New Manhattan Project goes, that’s about all you need to know.

The Travelers

Historically, when it comes to weather and the modification thereof, the Travelers Insurance Corporation of Hartford, Connecticut has been the most active insurance company.

Weather related financial instruments have been pioneered by the Travelers. As early as 1954, in co-operation with the U. S. Weather Bureau, the Travelers simultaneously established a weather research organization called The Travelers Weather Research Center and a weather observing and forecasting station called The Travelers Weather Service. A radio station owned by the insurance company disseminated weather information to the public. Information was also shared with government groups. An associate professor of meteorology from the Massachusetts Institute of Technology named Thomas F. Malone headed these operations. At the time, the president of the company said, “This action is being taken after long and thorough investigation of the possibilities of weather study in relation to insurance underwriting.”

In the early 1960s, the Travelers participated in the Bureau of Reclamation’s massive Project Skywater.

By 1967, the Travelers had studied the large-scale hydrology of North America east of the Rockies with the Environmental Science Services Administration (ESSA); the predecessor to today’s National Oceanic and Atmospheric Administration (NOAA).

In 1968 it was reported in the proceedings of the tenth NOAA weather modification conference that the Travelers was paid by the National Science Foundation (NSF) to review the NSF’s weather modification documents in order to, “…investigate the possibility of abstracting useful scientific information….”

In 1968, the NSF reported that,

- Quote :

- The Bureau of Reclamation has initiated a project with the Travelers Research Center in Hartford, Conn., to formulate a simple model to study the effects of artificial nucleation over relatively large areas and the feasibility of surface or aircraft seeding. The qualitative value of precipitation augmentation over the Connecticut River Valley has now been established with respect to municipal water supply, pollution abatement, power generation, and recreation.

The icing on the cake here is that the Travelers insured the original Manhattan Project. Let us refer to a 1964 self-produced history.

The Travelers: 100 Years reads:

- Quote :

- The Travelers was approached by the private contractors engaged in the project with the request that the Companies administer the forms of insurance which would be required to protect workers and the public. The Companies assented, on the condition that the government guarantee the payment of premiums. This done, a special underwriting formula was worked out.

Not only did the Travelers provide the Manhattan Project insurance, they also did a good job covering it up.

The Travelers: 100 Years continues:

- Quote :

- The most ticklish phase of the adjustment of claims was the necessity of keeping them from reaching law courts, where publicity might have drawn undesired attention to the mysterious operations in process at Oak Ridge and Hanford.

The Travelers (as many other insurers) has since gone on to provide lots of insurance for the nuclear power industry.

Weather Derivatives

Since the heady days of the Travelers’ first excursions into weather related financial products, other weather related financial markets and products have arisen. The first of two markets to be discussed here is the weather derivatives market. The other market is the catastrophe reinsurance market which will be discussed shortly.

In his paper “Why in the World Are They Spraying?,” journalist Michael Murphy floated the idea that chemtrails are sprayed (at least in part) in order to manipulate the weather derivatives market. He posted his story in October of 2011. He may not be too far off the mark as an investigation detailed here leads us to many questionable situations, strange bedfellows and none other than those legends of corruption and waste, Enron. The thoroughly disgraced and vilified corporation was the founder of the market. Would you put it past Enron?

Weather derivatives are financial instruments (options, futures, and options on futures) anyone can buy that either pay off or don’t pay off according to recorded atmospheric conditions such as temperature and rainfall. These instruments are mostly traded on the Chicago Mercantile Exchange (CME). They are also traded on smaller ‘over the counter’ (OTC) markets. Weather derivatives are usually structured as swaps, futures, and call/put options.

Although they are available for sunshine hours, snowfall, rain, wind speed and many other geophysical conditions, the most common type of weather derivative by far is based on temperature. According to industry experts, temperature based weather derivatives account for 75-99% of all weather derivatives sold. Atmospheric conditions are recorded and published by authorized organizations.

This is how temperature based weather derivatives work. Indices take a location’s daily average temperature, then a number is determined by how much that day’s average temperature deviates from 65 degrees Fahrenheit (or 18 degrees Celsius outside the U.S.). The number deduced determines the derivative’s value and can be aggregated over a period of hours, days, weeks, months or seasons. Other indices simply aggregate average daily temperatures. In short, the day’s average temperature determines the derivative’s value. You can bet that temperatures will be above or below the long term daily average for a particular hour, date or group of dates.

The first weather derivative transactions were conducted over the counter in 1997 between Willis Group Holdings, Koch Industries, Pxre Reinsurance Company and Enron. These transactions followed the deregulation of the energy market in the United States.

The weather derivatives market was greatly expanded in 1999 when weather derivatives began trading on the Chicago Mercantile Exchange.

The leading weather derivatives industry association was founded in 1999 and is called the Weather Risk Management Association (WRMA). According to former Enron employee Lynda Clemmons, “The Weather Risk Management Association was launched by myself, and by Jim Gosselin of Castlebridge Partners, Darren Wilcox of Southern Co., Ravi Nathan of Aquila Energy and Jeff Porter of Koch Industries.” Mrs. Clemmons neglected to mention another WRMA founder, Swiss Re.

In 2011, the WRMA released the results of a survey which pegged the current global weather derivatives market value at about $12 billion.

USA Today says in their article “Weather Derivatives Becoming Hot Commodities” that the largest broker of weather derivatives in the world is TFS Energy. A man named Kendall Johnson, who is described as one of the industry’s most powerful professionals, states, “Businesses in the U.S., Japan, London and Amsterdam are the most frequent users of weather risk management, though companies in emerging markets like India are beginning to trade weather derivatives.”

Other big corporate players include: Aquila Energy, Southern Energy, Castlebridge Weather Markets, British Gas, Hess Energy, ABN Amro, Merrill Lynch, AXA Re, Swiss Re, Koch Energy, RenRe Energy, Nephila Capital, Munich Re, Speedwell Weather Derivatives, Vyapar Capital Market Partners, Galileo Weather Risk Management, PCE Investors / Cumulus, EDF Trading Limited, Risk Solutions International, E.ON Energy Trading, Mitsui Sumitomo Insurance Company and Endurance Reinsurance Corporation of America. As you can see, re-insurers are some of the biggest market players.

Swiss Re is a name that comes up again and again, and just happens to be the insurer of the World Trade towers at the time of the 9/11 attacks. But, that’s surely just a coincidence. There’s nothing to see here. Move along.

Swiss Re also happens to be the purchaser of General Electric’s reinsurance company Employers RE. Although General Electric scientists famously started the New Manhttan Project in 1946, we can rest assured that Swiss Re is not involved. Read all about it

here.

The energy sector is the biggest buyer of weather derivatives because energy companies’ bottom lines and cash flows are largely affected by temperature fluctuations. This is why temperature based weather derivatives are the most prevalent. Energy companies produce more power and thus increase cash flows when the weather gets either hot or cold because people use more air conditioning when it is hot and more heat when it is cold.

The weather derivatives market was created with the energy sector in mind. As we have seen, the market was founded by big energy players, most notably Enron. According to a Chicago Mercantile Exchange brochure, the 65 degree baseline selected for determining daily index values was chosen by the energy industry. The terms used to describe index values are Heating Degree Days (HDD) and Cooling Degree Days (CDD). Heating Degree Days refer to the number of degrees Fahrenheit above 65 the average temperature of a winter’s day is. Cooling Degree Days refer to the number of degrees Fahrenheit below 65 degrees a Summer’s day is. It is this way because 65 degrees is about the temperature where if it is warmer than that, people use more air conditioning and if it is cooler than that, people tend to use more heating.

Industry publications claim substantial non-financial or non-energy sector participation in the weather derivatives market. Of businesses outside the finance or energy sectors, this investigation revealed very little participation. It is unrealistic that, especially in the tough economy we’ve been having lately, an organizer of an outdoor event, let’s say, would first of all even be aware of weather derivatives, much less use the time, energy, expertise and money to buy such things. Businesses outside of finance and energy usually use more traditional forms of insurance or hedge with commodities contracts. Weather derivatives are almost entirely an energy and finance sector market. There is hardly any retail investor activity here, if at all.

Industry publications also often claim that weather derivatives are used by energy companies only as hedges against unforeseen demand lapses. If a particular Winter is too warm, for example, an energy company would not make as much money selling fuel as they would in an abnormally cold Winter. But, the reasoning goes, if they have purchased a hedge in the form of weather derivatives, they can make up those losses.

Weather derivatives are traded like any other Wall Street market. To make a buck, they are traded any way possible. Enron, the founder of the market, is famous for their trading desk which specialized in arbitrage. Because weather derivatives, energy futures and energy company revenues rise and fall depending upon temperature, the markets are related. This is why weather derivatives are often traded in conjunction with energy futures.

The 2007 Bloomberg article “Hedge Funds Pluck Money From Air in $19 Billion Weather Gamble” had it right. Nowhere in this article will you see any mention of non-financial or non-energy sector participation. In fact, industry professionals are quoted as saying they are, “…using weather as market intelligence.” And that their business is, “…like playing poker.”

Or consider Enron’s John Sherriff, an originator of the market. According to Risk.net Magazine:

- Quote :

- He decided to sit out on the trading floor rather than in an office and other managers followed his example, including the company lawyer. ‘I was an advocate of sitting on the trading floor,’ says Sherriff. ‘For a start, I found it the most exciting place in the building, but I also wanted to be accessible. I thought it would create an environment where there was more and quicker communication.’

Mr. Sherriff was apparently quite the gambling man. The Authors of

The Smartest Guys in the Room write:

- Quote :

- The Sherriff legend was that he had made an enormous amount – tens of millions – in a single bet on short-term gas prices back in the mid-1990’s, when the business was still in its early stages and such a windfall was not believed possible.

Stories about the gamblin’ John Sherriff seem to go on and on. Also from

The Smartest Guys in the Room we find:

- Quote :

- Every year on the annual retreat to the Hyatt Hill Country Resort in San Antonio for vice presidents and above, a group of traders would play a poker game called Omaha (where the lowest hand and the highest split the pot) at the same table in the lobby of the hotel. The pot was usually around $1,000, but in the final year it was played – 2000 – three players thought they had good odds of winning. The pot grew to $33,000, as the crowd gathered and the tension built into the early morning hours. One player had both the high hand and the low hand. He bought a new BMW. The other two – one of them London chief John Sherriff – were out $11,000 each.

Weather derivatives by themselves are big money gambles. They probably contribute to making it worthwhile to put planes up in the sky spraying stuff on a daily basis. If you divide 2011’s total market value ($12 billion) by the number of traded contracts (466,000), you get the average contract value which is $25,321. A matter of a few degrees on a given day or group of days could mean hundreds of thousands of dollars.

The weather derivatives market and other opportunities were made possible by deregulation of the energy market. Enron founded the weather derivatives market. Deregulation necessarily means government involvement. Was the Department of Energy in bed with Enron? As we will see in the next section, Enron CEO ol’ Kenny Boy (as the Bushes called him) had extensive experience and connections with energy policy at the Federal level.

The fact that Enron founded the weather derivatives market is very dubious. This is a company whose accounting firm, Arthur Andersen, shredded more than a ton of their documents in one day as Enron’s chairman Ken Lay told everybody everything was fine. When Enron divisional CEO Lou Pai’s wife found out about his stripper girlfriend complete with his love child, she divorced him. Enron’s bankruptcy resulted in criminal charges against at least 21 former executives. People suffered under high power costs inflated by Enron. When Enron and their cronies intentionally disrupted power service as they were known to do, people were injured and died. Who knows how many bodies they left behind? These guys were not playing Tiddlywinks. We shouldn’t put anything past Enron.

A History of Weather Derivatives

Lots of information about the history of the weather derivatives market is available. It is this way because Enron originated the weather derivatives market. The fall of Enron was one of the greatest corporate scandals in American history, so there has been much already investigated and exposed. This section examines this history of weather derivatives so inextricably connected to one of the most famously dishonorable corporations in history.

When you’re talking about the history of weather derivatives, you’re talking about Enron. They developed the most widely used early trading platforms, they were founding members of the leading industry association and were counterparties in the first known domestic and international transactions.

In their heyday, Enron received Fortune Magazine’s award for ‘Most Innovative Company’ six years in a row. They gave their Enron Prize for Distinguished Public Service to people like Nelson Mandela and Mikhail Gorbachev. Henry Kissinger and James Baker worked as Enron consultants; traveling to such far-flung destinations as Kuwait and China preaching the Enron gospel. Stock analysts gushed over everything Enron did. Enron could seemingly do no wrong.

The only problem was, Enron was cooking the books seven ways to Sunday. When the S.H.T.F., Enron’s stock tanked like World Trade Center building 7 and eventually brought down one of the nation’s oldest and largest accounting firms, Arthur Andersen.

Although the company itself has long since been chopped up and sold off, former Enron employees now populate many other financial market trading establishments.

***

The particular division known to buy and sell weather derivatives was called ‘Enron Weather.’ Enron Weather started as a small, but promising bit of the company. By the time of Enron’s demise in 2001, Enron Weather had grown to a significant part of their business.

Although the book

What Went Wrong at Enron claims that the weather derivatives market probably came from an idea that just popped into the head of the TV weatherman brother of Enron executive Jeffery Skilling, there is quite a bit of documented history long before this. From a 1968 example, we learn that the National Science Foundation (NSF) was laying the foundations of the weather derivatives market a long time ago. The tenth annual NSF weather modification report reads:

- Quote :

- Under NSF support, the University of Missouri is continuing its study of a method to determine the potential impact of weather and climate modification upon the social and economic structure of a sample State such as Missouri. The electrical power industry has been considered to be one which is both weather sensitive and one for which data useful for statistically isolating this relationship are available. For this reason it was decided to make study of the potential effects of weather modification on its operation. Daily electrical power demand data covering a number of midwestern states were supplied by the Edison Electric Institute.

Using these data and Weather Bureau temperature records, it was possible to construct a series of power loads for each of a number of regions in the study area corresponding to the modified and nonmodified temperature series. Power generation costs and capacities for each of the regions in the study area were then entered into a linear programming model. With the modified and nonmodified load series, it was possible to construct two estimates of the cost of supplying power to the area. Each area power supply cost was a minimum given the loads and existing generation facilities. Comparisons of the costs of supplying power to the area during the summer months then provided an estimate of the direct effect of potential temperature modification on the electrical industry.

The ‘degree day’ term and the 65 degree threshold are discussed as early as 1975 in “Economic Impacts of Weather Variability” by James McQuigg.

Expanding upon the degree day thesis, the 20th ICAS report reads,

- Quote :

- …CCEA

is developing highly sophisticated mathematical models by which population-weighted degree days can be linked specifically to use of natural gas, to the exclusion of other fuels.

Although many others had previously laid the groundwork, it wasn’t until the late 1990s that Enron entered the picture. Loren Fox, the author of

Enron: The Rise and Fall tells the story of Enron Weather like this:

- Quote :

- …weather derivatives came to be championed by an employee working at the grassroots level and seeing customers’ daily needs. John Sherriff, who at the time managed gas trading for the western United States, began looking at derivatives linked to the weather in late 1995, and Vincent Kaminski’s research group worked on the idea in 1996. A gas trader named Lynda Clemmons was very interested in the idea, based on her conversations with executives at electric utilities that used coal-fired power plants…. In 1997, Enron handed off its weather derivatives effort to Clemmons, who was only 27. She began a one-person weather-hedging department within ECT [Enron Commodities Trading]…

Fox continues:

- Quote :

- …Clemmons built up Enron’s weather business so that it did 350 transactions (hedging up to $400 million in potential revenues) in 1998, turning its first profit that year.

Enron initiated the weather derivatives market in Europe as well. Enron’s Oslo office became the base of their European weather derivatives business. In 2000, Enron also introduced weather derivatives in Australia; offering temperature-based products for Sydney, Melbourne, Hong Kong, Tokyo and Osaka.

In 2002, after the bankruptcy, the Enron trading desk (including Enron Weather) was bought by UBS Warburg.

According to his websites, John Sherriff is now the owner of Lake Tahoe Financial and other Sherriff family businesses.

Mrs. Clemmons left Enron in 2000. She took a number of her colleagues from Enron’s weather team and set up weather derivatives company called Element Reinsurance. After Enron, Lynda Clemmons also worked at XL Weather & Energy, The Storm Exchange Inc. and Vyapar Capital Market Partners. According to her LinkedIn profile, Mrs. Clemmons is now an independent consultant.

***

The Enron financial market trading desk, just like the company itself, had a history of corruption. Back in 1987, the Enron trading operations were called ‘Enron Oil.’ When questions about an Enron account at New York’s Apple Bank began surfacing, Enron management turned a blind eye. Money was pouring into this questionable account from a bank in the Channel Islands and flowing out to the account of a man named Tom Mastroeni; the treasurer of Enron Oil.

Enron management explained away these money flows and this questionable account as completely legal profit shifting. Although Mastroeni produced doctored bank statements and admitted a cover-up, Enron management didn’t pursue the issue. Nobody involved was even reprimanded. Revelations continued to come out, but Enron management did nothing. Enron’s accounting firm Arthur Andersen exhibited a similar disinterest.

After management confirmed an official lack of responsible oversight, Enron Oil traders ignored position limits and got themselves in big trouble. Only then did Enron executives show interest.

The authors of

The Smartest Guys in the Room tell the story like this:

- Quote :

- For months, Borget [the CEO of Enron Oil] had been betting that the price of oil was headed down, and for months, the market had stubbornly gone against him. As his losses had mounted, he had continually doubled down, ratcheting up the bet in the hope of recouping everything when prices ultimately turned in his direction. Finally, Borget had dug a hole so deep – and so potentially catastrophic – that there was virtually no hope of ever recovering.

Enron brass was in a panic. Enron was looking at a $1 billion loss; enough to bankrupt the company. Management sent in some expert traders who, over the course of a few weeks, managed to clear out these positions with only a $140 million loss.

Enron had to tell people about this $140 million trading loss, though. Enron’s stock slid 30%. The blame game began. Ken Lay, the affable Enron founder and CEO, denied any responsibility. News of the scandal conveniently came out right after a big bank loan approval.

The U.S. attorney’s office charged Borget and Mastroeni with fraud and personal income tax violations. In 1990, Borget pled guilty to three felonies and was sentenced to a year in jail and five years’ probation. Mastroeni pled guilty to two felonies. He got a suspended sentence and two years probation.

***

Ken Lay created new financial markets (such as the weather derivatives market) and helped his company make more money through energy sector deregulation. Deregulation created a situation where Enron and others could more effectively manipulate and arbitrage (specifically regulatory arbitrage) markets.

Let us refer to a feature article published by industry publication Risk.net:

- Quote :

- ‘Enron was the focal point of the deregulation agenda,’ says Jonathan Whitehead, who started with Enron Europe in 1996 and was heading the liquefied natural gas (LNG) business in Houston at the time of Enron’s demise. ‘It was the most vocal when explaining to regulators and governments and customers the benefits of deregulated markets. I don’t think deregulation in power and gas in Europe or the US would have come as far as it has without Enron,’ he says.

Pushing for deregulation was very much a part of the company’s strategy from the start. ‘Ken Lay [chairman and chief executive of Enron] was the visionary at the time as far as seeing where deregulation could go and actually driving deregulation,’ says Mark Frevert, who worked at one of Enron’s predecessor companies, Houston Natural Gas, from 1984 and stayed at Enron until it’s demise.

Deregulation necessarily required help from the federal government. To make it happen, Enron and Ken Lay (who died in 2006) had the right federal connections in spades.

Ken Lay enlisted in the navy in 1968. His friend pulled some strings and had him transferred to the Pentagon. According to the authors of

The Smartest Guys in the Room, Lay spent his time at the Pentagon, “…conducting studies on the military-procurement process. The work provided the basis for his doctoral thesis on how defense spending affects the economy.” Ken Lay had many high level military connections. The evidence suggests that domestic chemtrail spraying operations are carried out by what passes for our military.

Mr. Lay had the right political and specifically energy related political connections as well. He worked in the Nixon administration as a Federal Power Commission aide, then as deputy undersecretary of energy in the Interior Department. As chairman and CEO of Enron, he sat on the boards of prestigious Washington DC think tanks and often traveled to Washington.

A revolving door existed between Enron and the federal government. Enron executive Tom White left the company to join the Bush Jr. administration as secretary of the army. Enron executive Herbert ‘Pug’ Winokur was Lay’s old Pentagon friend. Robert Zoellick (now Chief Executive at the World Bank) worked for Enron, then became a United States Trade Representative and later the Deputy Secretary of State.

According to the authors of

The Smartest Guys in the Room, “In 1993, Lay added Wendy Gramm [to the Enron board], who had just finished a stint as chairman of the Commodities Futures Trading Commission (CFTC) and was married to Texas Senator Phil Gramm.” It continues, “Just after Wendy Gramm stepped down from the CFTC, that agency approved an exemption that limited the regulatory scrutiny of Enron’s energy-derivatives trading business, a process she had set in motion.”

When Enron galloped into Europe, they had an influential lord on their side. Journalist Greg Palast covers it like this:

- Quote :

- The fact that a truly free market [in electricity] didn’t exist and cannot possibly work did not stop Britain’s woman in authority, Prime Minister Margaret Thatcher, from adopting it. It was more than free market theories that convinced her. Whispering in her ear was one Lord Wakeham, then merely ‘John’ Wakeham, Thatcher’s energy minister. Wakeham approved the first ‘merchant’ power station. It was owned by a company created only in 1985 – Enron. Lord Wakeham’s decision meant that, for the first time in any nation, an electricity plant owner, namely Enron, could charge whatever the market could bear… or, more accurately, could not bear.

It was this act in 1990 that launched Enron as the deregulated international power trader. Shortly thereafter, Enron named Wakeham to its board of directors and placed him on Enron’s audit and compliance committee.

***

A scheme to manipulate financial markets by modifying the weather would necessarily involve intelligence agencies. According to the authors of

The Smartest Guys in the Room, Enron had intelligence agency connections:

- Quote :

- One of Enron’s key advantages over its competitors was information: it simply had more of it than its competitors. It’s physical assets provided information, of course. And Enron didn’t stop there. It employed CIA agents who could find out anything about anyone. In stead of tracking the weather on the Weather Channel, the company had a meteorologist on staff. He’d arrive at the office at 4:30 A.M., download data from a satellite, and meet with the traders at 7:00 A.M. to share his insights.

It continues,

- Quote :

- By the late 1990’s, these research efforts were herded together into something called the fundamentals group – fundies in trader parlance. The fundies group produced intelligence reports and held morning briefings…

***

Mr. Lay and Enron had many connections to the Bush family and their cohorts. President George W. Bush (Bush Jr.) lovingly called Ken Lay ‘Kenny Boy.’ Mr. Lay was also close to his father, fellow Houstonian, George H.W. Bush (Bush Sr.). For example, in 1991, Bush Sr. offered Mr. Lay the position of Commerce secretary. Mr. Lay turned him down. He wanted to be Treasury secretary.

Greg Palast, in his book

The Best Democracy Money Can Buy, characterizes the Bush/Enron relationship like this:

- Quote :

- But what about Pioneer Lay of Enron Corp? His company, America’s number one power speculator, was also Dubya’s number-one political career donor ($1.8 million to Republicans during the 2000 presidential campaign). Lay was personal advisor to Bush during the postelection ‘transition.’ And his company held secret meetings with the energy plan’s drafters. Bush’s protecting electricity deregulation meant a big payday for Enron – subsequent bankruptcy not withstanding – sending profits up $87 million in the first quarter of Bush’s reign.

Other Bushes were apparently getting some, too. Greg Palast writes,

- Quote :

- Two months after the bankruptcy, Governor Jeb Bush of Florida traveled to the Texas home of Enron’s ex-president, Rich Kinder, to collect a stack of checks totaling $2 million at the power pillager’s $500-per-plate fund-raising dinner. There are a lot of workers in Florida who will wish they had a chance to lick those plates, because that’s all that’s left of the one-third of a billion dollars Florida’s state pension fund invested in Enron – three times as much as any other of the fifty states.

Mr. Palast continues,

- Quote :

- Governor Bush encouraged a scheme by a company called Azurix to repipe the entire Southern Florida water system with new reservoirs that would pump fresh water into the swamps. From the view of expert hydrologists, such a mega-project is a crackbrained and useless waste of gobs of money. As part of the deal, Azurix would be handed the right to sell the reservoir’s water to six million Florida customers. Azurix was the wholly owned subsidiary of Enron that had recently been kicked out of Buenos Aires.

Specializing in private equity buyouts, The Carlyle Group is one of the Bushes’ two main family businesses and one of the nation’s largest defense contractors. Evidence suggests that chemtrail spraying is a military operation. The Carlyle Group could help geoengineering programs happen.

Participation in a scheme to defraud the population while murdering them at the same time would probably be A-Ok. with the Bush family. Bush family members exhibit recurring criminal behavior. Forget about the Enron connections. Do you know about the Nazi connections? Are you aware of the numerous links to 9/11? Have you heard of the connections to the attempted Reagan assassination or the attempted assassination of Pope John Paul II or the JFK assassination? Don’t forget that little Iran-Contra fiasco and the drug dealing, gun running and money laundering. Yup, they’re connected to that dirty, dirty BCCI thing, too. Folks, these are just some of the things we know about. When you see a few cockroaches, you can bet there are hundreds more in the wall.

So, who funds the Bush family? The answer is a little investment bank called Brown Brothers Harriman. Maybe you’ve heard of it. This is the American bank that funded the Nazi war effort during WWII. Webster Tarpley and Anton Chaitkin in their book

George Bush: the Unauthorized Biography describe the situation like this,

- Quote :

- For George Bush, Brown Brothers Harriman was and remains the family firm in the deepest sense. The formidable power of this bank and its ubiquitous network, wielded by Senator Prescott Bush up through the time of his death in 1972, and still active on George’s behalf down to the present day, is the single most important key to every step of George’s business, covert operations and political career.

In short, the Bush family, Enron and Ken Lay had the right political, business, intelligence and military connections necessary to facilitate the scheme outlined here.

***

Enron was a business laboratory. In the new world of deregulation created by the Bushes, Enron and others, the purpose of the company was to throw things against the wall and see what stuck. Enron was the perfect environment in which to try something new like weather derivatives. In light of the histories of corruption exhibited by those involved, it is understandable that the weather derivatives market they created may have been part of yet another murderous rip-off.

While most financial market trading operations are seen as unreliable, Enron’s trading desk was often regarded as their most productive and stable business. Could this have been because they were getting inside information about weather produced by geoengineering activities? They had the ways and means necessary. Enron had motive and opportunity. Enron benefited from weather derivatives.

Catastrophe Reinsurance

Besides weather derivatives, there is also another, larger financial market which rises and falls with the weather; the catastrophe reinsurance market. In this market, the most commonly issued security is something called a ‘catastrophe bond.’ The issuance of catastrophe bonds themselves is a bespoke market. That means participants engage in direct and often lengthy negotiations to craft customized agreements.

The weather derivatives market and the catastrophe reinsurance market are part of a larger market known as the ‘Alternative Risk Transfer’ market. The Alternative Risk Transfer market is an insurance market. ‘Risk transfer’ is insurance.

You may have heard of the catastrophe reinsurance market. It’s home to the ‘terrorism insurance’ market. The catastrophe reinsurance market is also home to the Special Contingency Risk (Kidnap & Ransom) market. Don’t forget the death bond market; you stand to gain healthy rates of interest if a certain number of people don’t die. But if they do, you lose and the banks get all your money, capiché?

Catastrophe insurance derivatives market participants come together at the New York based Catastrophe Risk Exchange (CATEX). Industry expert Erik Banks describes it like this,

- Quote :

- Although CATEX is not a formally regulated exchange and does not trade standardized contracts, it brings together multiple parties in a central forum so that they can execute cat risk covers in a organized fashion. In practice, participants (who must be subscribers) make use of CATEX’s technology platform to post exposures they seek to cover or protect. Once posted and matched, the two parties conclude discussions in a private setting; CATEX might therefore be regarded as a hybrid listed OTC transaction-matching conduit.

Once issued, these catastrophe bonds (or ‘cat bonds’ as they are called) are then cut into little pieces and sold in a process known as ‘securitization.’ Insurance Catastrophe Futures Contracts have been trading on the Chicago Board of Trade (CBOT) since 1992.

If a bank or insurance company wants to position themselves to gain a whole lot of money in the case of a series of catastrophic hurricanes in a particular region, let’s say, or a certain region suffering a sustained draught or floods or tornadoes or earthquakes, that’s what the catastrophe reinsurance market is for.

Although catastrophe bonds have only been around since the early 1990’s, the catastrophe reinsurance market has been around since the 1960’s. The leading industry association was founded in 1968 and is called the Reinsurance Association of America (RAA). The RAA describes itself thusly,

- Quote :

- The RAA is committed to promoting a regulatory environment that ensures the industry remains globally competitive and financially robust, unhindered by conflicting state and federal regulation.

The RAA’s public policy priorities include: federal and state financial role for natural disaster and terrorism catastrophe risk; regulatory reform efforts at the federal and state level; international trade, accounting and tax policy; accounting and financial reporting; solvency oversight and reinsurance recoverables; and climate change and environmental risk.

***

The catastrophe reinsurance market involves much more money than the weather derivatives market. While the Weather Risk Management Association recently pegged the value of the global weather derivatives market at about $12B, industry player Nephila Capital’s website states, “The amount of notional exposure that trades in the catastrophe reinsurance market each year is approximately $200B.” Now we’re talking about your ‘disaster capitalism’ industry!

2011 was a big year for the catastrophe reinsurance market. In September of 2011, the industry’s biggest broker Guy Carpenter released a report stating, “The devastating earthquakes in New Zealand and Japan, along with damaging tornadoes and floods in the United States and Australia, have resulted in insured losses of around USD70 billion so far this year.”

Munich Re puts 2011 industry losses for the first half of the year at $265 billion; easily surpassing the previous full-year record amount of $220 billion set in 2007. According to Munich Re, “The 9.0 magnitude earthquake, the strongest ever registered in Japan, is also the costliest natural catastrophe on record.”

The size of this market is much greater than the potential cost of chemtrail operations. In congressional testimony, geoengineers estimate the total yearly cost of ‘full deployment’ for a stratospheric aerosol program utilizing jet airplanes at between, “a few billion dollars per year” to $10B. Aurora Flight Sciences did a cost analysis study in which they concluded that, using retrofitted Boeing 747s, it would cost $1B per metric ton of aerosols per year.

Financial and energy market deregulation enabled the existence of today’s catastrophe reinsurance and weather derivatives markets. Financially, the repeal of Glass-Steagall was key. Here is a passage from a book by industry insider Erik Banks, “In the US, product and market convergence has been aided by the passage of the 1999 Financial Modernization Act (i.e., the Gramm-Leach-Biley Act), which eliminated the 1933 Glass-Steagall Act and Depression-era legislation that prohibited banks and insurance companies from encroaching on each other’s territory.” When Mr. Banks refers to ‘convergence,’ he’s writing about money pouring into the insurance industry from the banking industry.

According to Mr. Banks, for tax and regulatory reasons, many catastrophe reinsurance industry participants choose to domicile in countries such as: Bermuda, the Cayman Islands, the British Virgin Islands, Luxembourg and Ireland.

***

The catastrophe reinsurance market consists of: related financial sector businesses, brokers, banks, hedge funds and insurance companies. None of the material this author read mentioned any retail investor participation. This is a professional insurance market.

Although industry consolidation remains a trend, related financial sector businesses such as Bermuda Transformers are needed to perform specific functions such as converting derivative instruments into reinsurance contracts. Brokers negotiate deals. The biggest brokers are Willis Group Holdings and Guy Carpenter & Company. Banks provide the capital. Big banks have internal hedge funds which play the catastrophe reinsurance market.

In this scenario, it makes sense that the catastrophe reinsurance market participants from the banking industry be big and corrupt. They need to be big because a lot of money is required. They need to be corrupt because the situation outlined here is a mass murderous rip-off. Those qualifications suggest the usual suspects: Bank of America, JP Morgan Chase, Citibank and the rest. If you don’t know that the big banks are corrupt by now, then may God have mercy on your soul. They launder the CIA’s drug money, OK?

Independent hedge funds such as Nephila Capital are also here to play. It seems quite odd that these people bet big money on something as presumably unpredictable as the weather. The circulations of our atmosphere are a good example of chaos. Who wants to bet big money on pure chaos? Maybe inquiring minds just think too much.

Insurance companies are here because they originated the market. The terms ‘insurance’ and ‘reinsurance’ are used here interchangeably because they are both essentially the same thing. Insurance companies sell catastrophe bonds and insurance-linked securities. Although many insurance companies issue catastrophe bonds and related securities, Swiss Reinsurance America Corporation and Munich Reinsurance America are the most prolific.

Many of the same companies which participate in the weather derivatives market also participate in the catastrophe reinsurance market. Since both markets rise and fall with the weather, it makes sense that they would. Here is a partial list of dual market players: Endurance Reinsurance Corporation of America, Nephila Capital, Swiss Re, Willis Group Holdings and Munich Re.

On a completely unrelated note, industry heavyweight Marsh & McLennan (who owns the industry’s biggest American broker Guy Carpenter) had all their World Trade Tower offices totally wiped out on 9/11. You see, Marsh & McLennan occupied floors 93-100. On the day of 9/11, the first plane completely gutted floors 93-99; killing every person on all of those floors.

Maybe somebody wanted to make sure certain people were taken care of. Maybe the target was some people on the 96th floor, which was direct center. Maybe guys from Afghanistan who didn’t know how to fly did it. Maybe it was Bigfoot, the Tooth Fairy or a purple dinosaur. 9/11 was an outside job and chemtrails do not exist. Stop thinking and please return to watching television.

A History of Catastrophe Reinsurance

Following a spate of presumably natural disasters occurring from 1991-1994, climatologist Stanley Changnon (1928-2012) served as the lead author of a 1996 report advocating for something resembling today’s catastrophe reinsurance market. Even though Changnon concluded that man-made global warming was probably not to blame, “Impacts and Responses of the Weather Insurance Industry to Recent Weather Extremes” suggests that finance and climatology should work with government in order to provide more protections for those affected by severe storms (catastrophes). This was when the big banks and the reinsurers initially converged and the catastrophe reinsurance market came into its own.

A passage from this report tells the story:

- Quote :

- The major storm losses of 1991-1993 created by 1993 a new level of interest built around a new theme: that the new extremes were a signal of a changed climate. Time [Magazine] and some trade journals carried articles about the hazard upsurge and its possible connection to a greenhouse-induced climate change (Linden, 1994). This concept was actively promoted by environmental interests who had a stake in the climate change issue and who claimed that the recent upsurge in catastrophes and record losses were ‘indicative of a change in climate due to the greenhouse effect’ (Leggett, 1993). They were joined by some atmospheric scientists who also claimed climate change was responsible for the upswing in losses since their calculations indicated that the greenhouse change would produce a climate with more storms, higher winds, and longer storm tracks (Rountree, 1994).

Leaders in the insurance industry began to consider the issue. Frank Nutter, President of the Reinsurance Association of America stated ‘the insurance business is first in line to be affected by climate change’ (Linden, 1994). Some insurance leaders, in assessing what factors had caused the recent (post 1990) upsurge in storm losses, included the possibility that climate change was a factor along with demographic shifts, growth of exposure, decaying infrastructure, and poor building codes (Lecomte, 1993; Berz, 1994). Certain insurance leaders claimed that climate change and the increase in storms were related, whereas others were not convinced (Viewpoint, 1995; Stix, 1996). Flavin (1994) addressed the key issues in a thorough analysis noting there had recently been a large number of storms, major recent increases in losses, and a vulnerable industry that became willing to believe that unique circumstance caused by a change in climate had occurred. Deering (1993) noted that those promoting concern over global climate change and a $1.8 billion U.S. research program, including environmental groups and atmospheric scientists, had acted to get the insurance industry to believe in climate change and thus to become allies on their side in promoting research and policy development relating to climate change. Over the last few years, the greenhouse-induced climate change issue has become a national and international policy issue with scientists, government bureaucrats, and policymakers arguing all sides of the issue (Flavin, 1994; Glantz, 1995).

This passage continues the story:

- Quote :

- Another financial result of the recent catastrophes was the expansion of the Bermuda-based reinsurance market (Jennings, 1995). The market was originally developed to create capacity and take advantage of the hard casualty market conditions of the 1980s, under the less restrictive regulations of the Bermuda government. After Hurricane Andrew, the Bermuda market saw the arrival of the ‘super cat’ reinsurers. These new companies were formed with different levels of capital, with most exceeding $300 million, and having the objective of providing a large participation in property catastrophe reinsurance programs. The capitalization of these companies was developed through public equity markets, private placements and investments by other insurance companies, reinsurance firms, investment banking firms, and insurance and reinsurance brokerage companies.

The report continues:

- Quote :

- CAT’s first started trading in 1992. Initially the traditional insurance and reinsurance market did not know how to react to the product. Segments of the market saw this as an unneeded form of compensation. Many felt that the shortage in catastrophe capacity would be solved in the traditional market, as the pricing of that product improved, and at first, CAT’s were minimally traded.

However, over the last three years, open interest in these contracts has risen steadily. In April 1993, only 61 contracts traded By January 1994, open interest was 4,800 contracts, and by August 1994, open interest exceeded 5,800 contracts. These futures contracts trade only on the floor of the Chicago Board of Trade (CBOT)…

Lastly, the report adds:

- Quote :

- In response to the need for increased catastrophe risk capacity, an Exchange has ben established in New York. In July 1995, the New York Insurance Department approved the licensing of a risk exchange facility to be domiciled and operated in that state. Catastrophe Exchange (CATEX), licensed as a reinsurance intermediary, was brought into existence through the efforts of the former Insurance Commissioner of New Jersey. It reflects interest in increasing capacity for the Long Island shoreline to obtain coverage against windstorm and beach erosion damage.

For this new CATEX, Enron’s now defunct accounting firm Arthur Anderson was slated to, “…establish an index that prices and rates exposures.”

A Comprehensive Plan

A massive global weather modification endeavor such as the New Manhattan Project requires that all the disparate motives outlined here need necessarily be folded into a comprehensive plan to manage the Nation’s and the world’s weather resources. This is how every aspect of weather related activity can be managed comparatively and simultaneously. This would be the best way to manage the New Manhattan Project’s socio-economic impacts. It is not a surprise that at least one such early study has been undertaken.

The 1966 book

Human Dimensions of Weather Modification featured a paper by James Hibbs titled “Evaluation of Weather and Climate by Socio-Economic Sensitivity Indices.” This paper outlines a comprehensive plan for managing the socio-economic impacts of a National weather modification program.

Under this plan, all socio-economic impacts of weather modification activities are categorized as being applicable to either ‘consumers’ or ‘producers.’ Consumers are defined as using weather services to, “…enhance values generated outside the market place. Personal enjoyment of leisure time and other non-income producing (in the dollar sense) activities are included. Also included are governmental actions using weather services to maintain or increase health, safety, general welfare, natural resource preservation, etc..”

The paper classifies producers as using weather services, “…for purposes of enhancing their professional, commercial or industrial activities. Thus, specialized services are used by professional meteorologists, agriculturists, commercial airlines and private business pilots, and marine transportation.”

Hibbs then goes on to describe a system of ‘measures of benefit’ applicable to all the defined groups potentially affected. His paper reads, “It appears feasible to develop indices suitable for use in decision-making based upon the aggregate of factors discussed in the previous section. A first effort has been made to use the concept of a generalized index of ‘weather influence’ combined with a dollar-weighted index of ‘benefit potential’ distributed among various weather influenced activities and within broad geographical areas.”

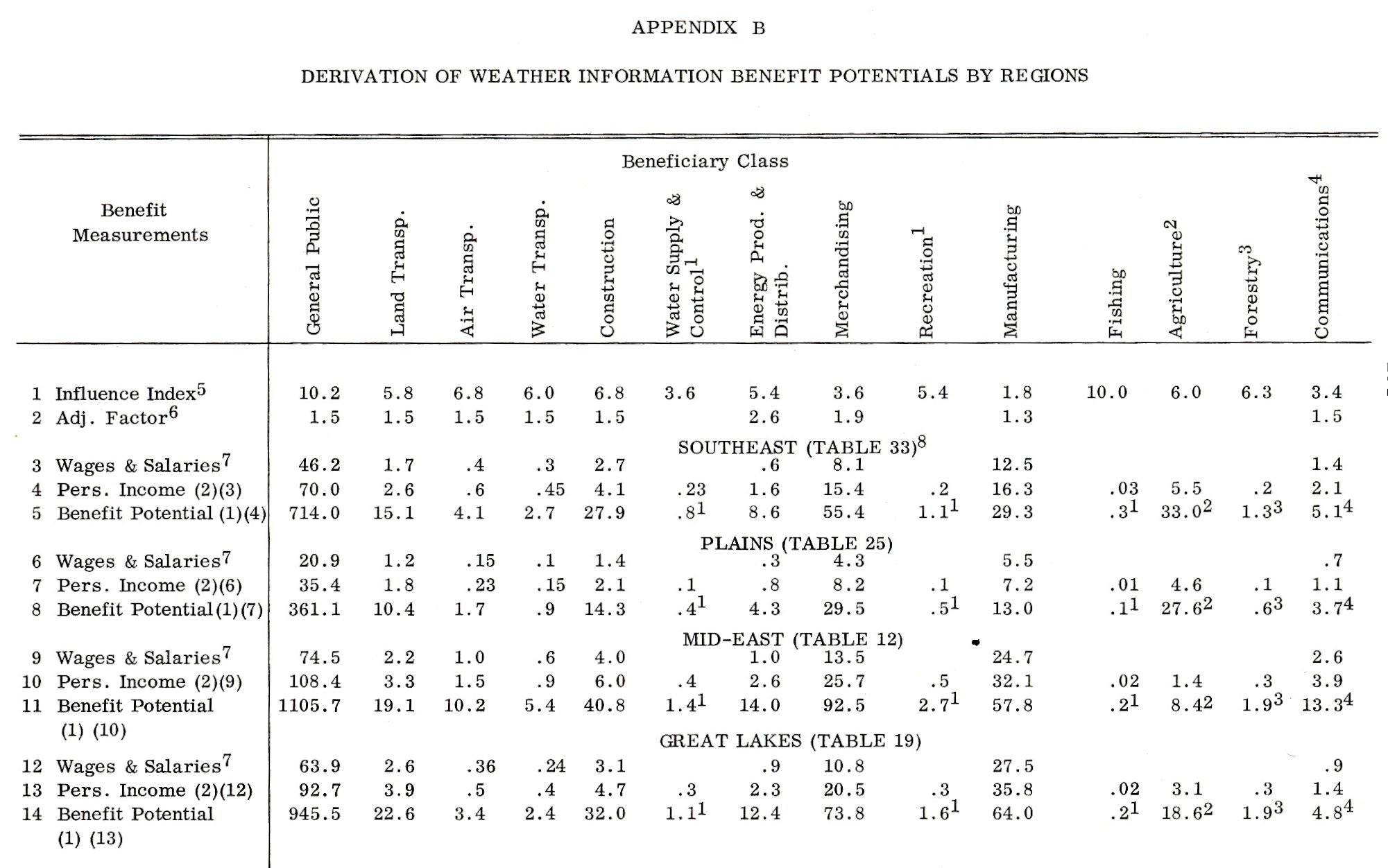

Weather sensitivity numerical table. Image source: University of Chicago / James R. Hibbs

Weather sensitivity numerical table. Image source: University of Chicago / James R. HibbsThe paper then goes on to quantify potential weather modification benefits by dividing the map of the United States into 8 regions. Each region is then assigned a numerical value representing four factors: the potential benefit for producers due to better weather forecasts, the potential benefit for producers due to weather modification, the potential benefit for consumers due to better weather forecasts, and the potential benefit for consumers due to weather modification. These values are to determine where and when different types of weather modification activities are to be conducted.

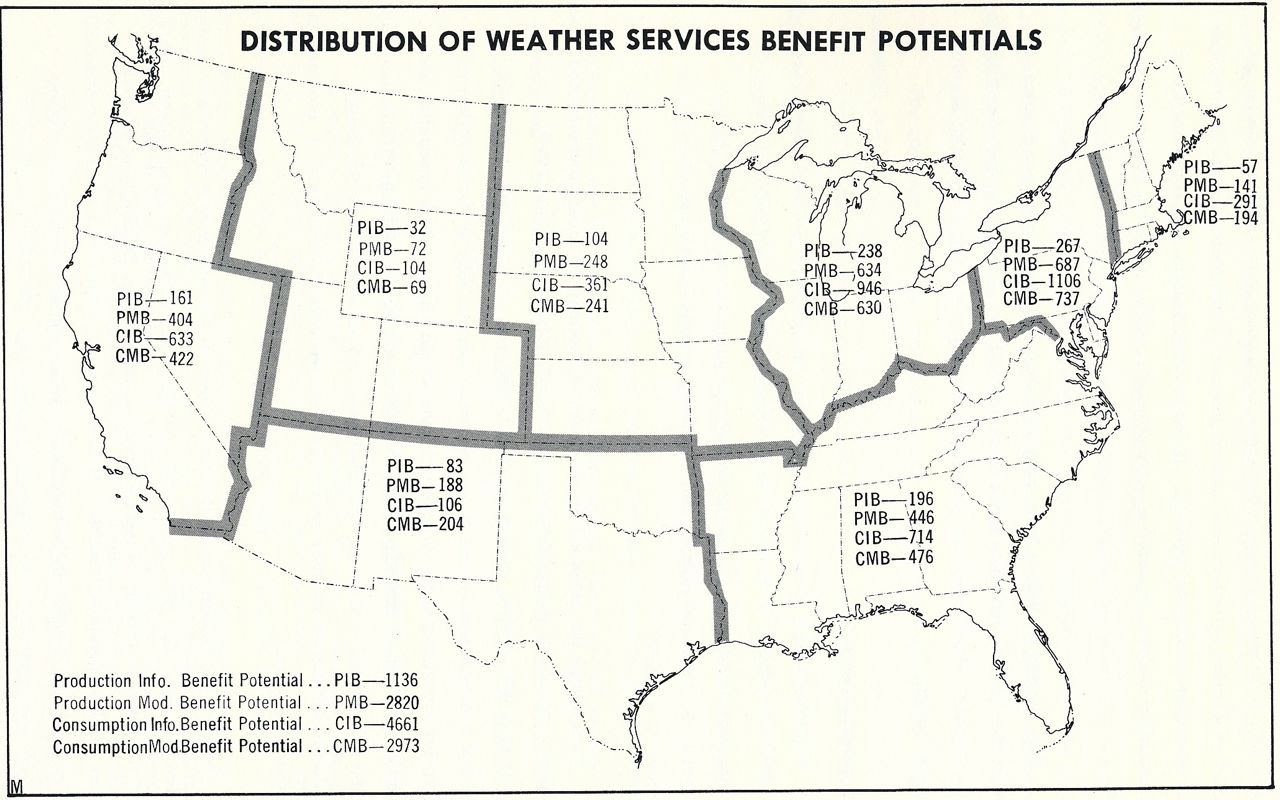

U.S. regions & weather sensitivity numerical values map. Image source: University of Chicago / James R. Hibbs

U.S. regions & weather sensitivity numerical values map. Image source: University of Chicago / James R. Hibbs“Evaluation of Weather and Climate by Socio-Economic Sensitivity Indices” discloses that the predecessor to NOAA, the Environmental Science Services Administration (ESSA) was developing these actuaries in order to aid ESSA policy and planning decisions. This suggests that NOAA manages the socio-economic impacts of today’s New Manhattan Project.

The paper concludes by noting, “The program would coordinate not only activities and available resources of many ESSA components, but also capitalize upon available resources and experiences within TAD-NBS, Census Bureau, Bureau of Labor Statistics, and NREC-OEP.”

Conclusions

Geoengineers will argue that all the motives presented here are precisely why we need a global weather modification project. They will argue that the Earth’s resources need to be better managed and that a global weather control program, producing better weather forecasts, allows for that. The truth is that we don’t need it or want it and we can’t trust the people doing it anyway.

We don’t need it. Humanity has been developing quite well for thousands of years without a global weather modification project. We need a clean environment, not one contaminated by geoengineering.

We don’t want it. We don’t want to breathe in the chemtrail witches’ brew and/or get zapped by this Project’s electromagnetic rays. Wether or not one realizes what is going on, these things are bad for us and our environment. Stop assaulting us!

We can’t trust the people behind it. Does a burglar ask for your permission before he robs your house? No. Does a mad military industrial complex ask you for permission before they ruin your health and wreck the environment? No, they don’t. The people responsible for this New Manhattan Project are not to be trusted. We don’t want to do business with them. These claims of deleterious Human health impacts and environmental devastation will be discussed shortly.

What we need is a system that does not allow the socio-economic elite to steal and hoard the Earth’s wealth as they spray us with chemtrails. We need a system that disallows the type of psychopathic gamesmanship currently going on. We need a system of government that cuts out the middlemen and delivers the wealth of the Earth directly to the people. We need the unequivocal enforcement of the American constitution and Bill of Rights. If this is achieved, there will be abundance for all and no want or need for any global weather modification project.

http://www.activistpost.com/2015/12/cui-bono-new-manhattan-chemtrail-project-motives.html?utm_source=Activist+Post+Subscribers&utm_medium=email&utm_campaign=3b7bc257d6-RSS_EMAIL_CAMPAIGN&utm_term=0_b0c7fb76bd-3b7bc257d6-387773073